Project Description

Borrowing to Invest via A Self Managed Super Fund

Changes to the superannuation legislation which came into affect September 2007 provided trustees of SMSFs with the opportunity to borrow for the purpose of acquiring a new single asset.

Trustees of SMSFs can purchase shares and property (commercial or residential – conditions do apply for monies transferred from UK Pensions) through their SMSF.

Providing the SMSF has a deposit and the proposed income means that meets the lenders loan valuation ration (LVR) requirements the lender will provide the balance of the purchase price. Banks may require a minimal deposit but trustees should be aware that negative gearing in a super fund is not tax effective due to the reduced tax rate applicable to super funds.

Limited Recourse Borrowing Arrangements (LRBA)

The Legislation requires that the loan must be a Limited Recourse Borrowing Arrangement (LRBA). This facility allows the lender to hold the property as security any existing or other assets held by the SMSF cannot be used as additional security. The lender may also require the members to provide personal guarantees.

Trustees can either borrow from a financial institution e.g. a bank or from a related party e.g. the members or an entity controlled by the members.

Structure

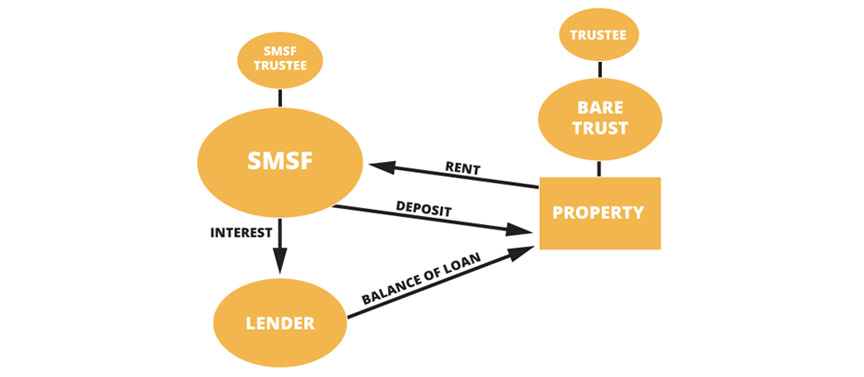

The Regulations require that the property acquired must be held by a bare trust with the SMSF being the beneficiary of the trust.

The bare trust is the registered holder of the property until the loan is repaid. The SMSF will receive rental income from the lessee and will pay interest to the lender.

If and when the loan is repaid the legal ownership of the investment property will revert to the trustees of the SMSF.

The trustees of the SMSF cannot be the same as the trustee of the bare trust, this may in some instances require a corporate trustee for both entities, this will be dependent on the lenders requirements.

Limited Recourse Borrowing Structure

Pitfalls to be aware of:

- Properties purchased with/or on multiple titles may need a separate bare trust for each property or title.

- Properties purchased using an LRBA cannot be significantly changed e.g. major renovations etc.

- Borrowings cannot be used to refinance an existing super fund property or improve / change an existing property held within the super fund.

- Believe incorrectly that super funds can borrow using the same strategies when borrowing personally or within a family trust structure (e.g. using existing unencumbered properties as security).

- Often sign a contract to purchase then seek advice.

- Execute the contract in the wrong name. As some states do not allow ‘and / or nominee’ clauses, this has the potential for additional stamp duty.

- Do not understand that the super fund must have cash to pay its share of the purchase price i.e. deposit.

- Want to borrow with little or no deposit.

- Do not understand that negative gearing does not work in a low tax (i.e. superannuation) environment.

- Forget that as trustees, investments are for the benefit of the members (not for the convenience of their business).